By JoAnn Kalenak, Senior Blogger —

For more than a year, I’ve listened as representatives from many worthwhile organizations deliver their pitch for financial help to Delta County’s Commissioners. Most have walked away with the same response, “Sorry, we don’t have the funds.”

Being among the poorest counties in Colorado, the Commissioner’s response seems understandable, that is until I began to dig deeper into the County’s 2018 proposed budget.

And, I’ve come away with more questions than answers.

Over the past several weeks, I’ve worked hard to understand the budget. The process and presentation has been fraught with opaque public notice and loads of mind-numbing spreadsheets.

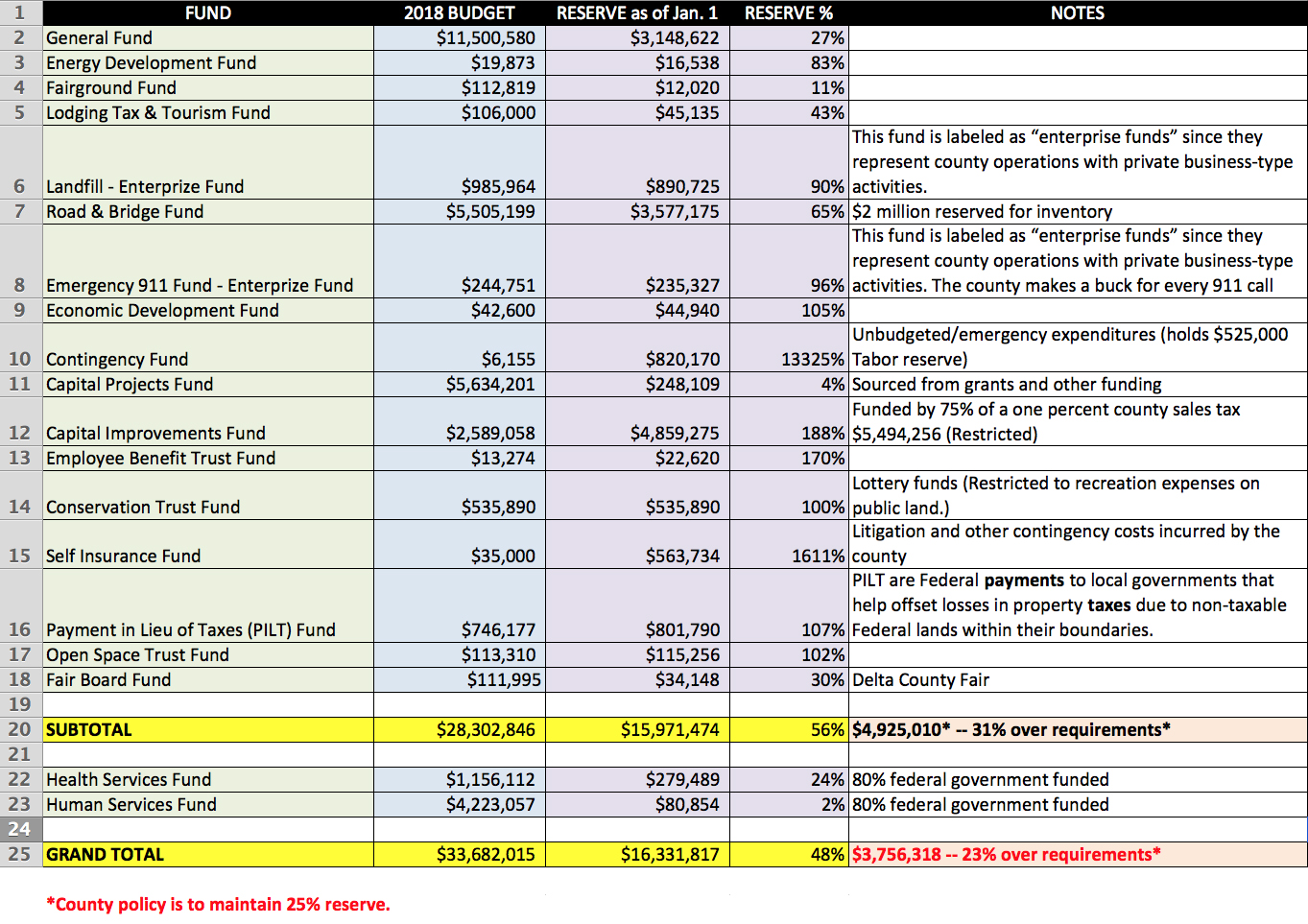

While neighboring counties and towns provide bountiful narratives and info-graphics in their budgets, Delta County’s budget consists of 95 rescanned balance sheets of all 17 funds and two proprietary funds (the landfill and emergency 911 calls).

THE IMPORTANT NUMBERS TO FOLLOW:

- Total proposed budget = $33,682,015

- Reserves left over from 2017 = $16,331,817

- Excess reserve = $3,756,318

{kind=link}

While the figures indicate that the County is certainly in the black, they also reveal that the County is carrying over 48% in reserve funds — 23% more than the 25% they generally shoot for, all without an allocation plan.

That’s more than $16,000,000 languishing in bank accounts earning less than one percentage interest, which is one and a half points below inflation.

Granted, governments can’t “gamble” taxpayer money by investing in riskier assets. The problem, however, is not banking or savings practices but that Commissioners have not publicly communicated any purpose for the excess reserve. Administrator Robbie LaValley commented in a budget meeting in September that the high reserves are “just in case.” However, as a point of County practice (not policy or resolution), the county already routinely holds a 25% reserve, which “…represents approximately three months of operating expenses, which is a generally accepted accounting best management practice,” adds LeValley.

The County further maintains a “contingency fund” for emergencies like fire or financial disaster to the tune of $820,170 in reserve funds (note: $525,000 is Tabor required reserve). And, in case the “regular” reserves and contingency funds are not enough, the County also maintains a $563,734 “self insurance fund” for litigation and other contingencies not budgeted.

Scott Olene with the Department of Local Affairs (DOLA) Budget and Finance office explained in a telephone conversation with me that while a reserve policy with minimum and maximum thresholds is not required by law (except the 3% TABOR reserve), best practices recommend such policies. DOLA also recommends that local budgets should include — among other details — a financial plan that explains why reserves are needed and how Commissioners plan to appropriate the funds. Olene emphasized that a budget is really a document meant for the public and should be designed with the layperson in mind.

Another fund I discussed with Olene was the Conservation Trust Fund (CTF), a project fund generated from lottery money strictly earmarked for recreation development on publicly owned land. For more than a decade, the County has maintained this fund’s reserve at almost a half million dollars. Since these funds are project dollars and not operational, there is little reason to maintain a reserve.

Olene concluded with a suggestion that it is ultimately the role of the public to demand transparency and fiscal responsibility from their elected officials.

I couldn’t agree more.

SPECIAL NOTE: The 2018 budget hearing is scheduled for Dec. 4 at 1:30 pm at the County Courthouse in Delta. Commissioners plan on adopting the budget shortly afterward at 3:30 pm. Pursuant to Colorado state statute governing local budgets: Any elector of the local government has the right to file or register his protest with the governing body prior to the time of the adoption of the budget.

National Advisory Council on State and Local Budgeting – Best Practices

Download 2018 Administration Budget Message